Recyclers feeling the strain as prices tumble

Iranpolymer/ Baspar The European recycled plastics market is under severe pressure because of extremely low demand and lengthening supply. While some recycling plants have been shut down, most others are operating at reduced rates in order to avoid excess stocks from developing. However, weak levels of demand mean that recyclers’ stock levels are steadily rising.

This situation applies to all recycled plastics sectors, but the situation is particularly precarious for PET recyclers where a fierce price war between R-PET and virgin PET means that it is very difficult to operate the recycling plants economically.

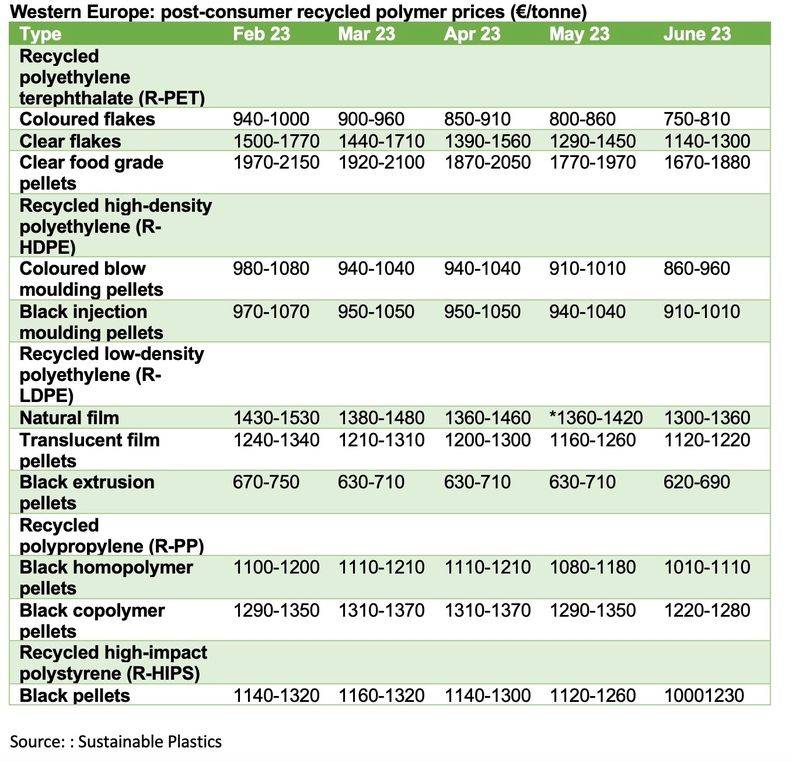

Despite a severe price reduction of €250/tonne for clear flake material and a fall of €200/tonne for clear food-grade pellets since the beginning of May, converters are increasingly switching to virgin PET where prices have tumbled in recent months. In mid-June, virgin PET prices were trading at €1150-1200/tonne compared to €1670-1880/tonne for clear food-grade pellets and €1140-1300/tonne for clear flake.

Recycled polyethylene terephthalate (R-PET)

R-PET prices have remained under heavy pressure over the last two months because of continuing weak demand, the lower cost of bottle scrap, competition from virgin PET and cheaper imported material. Clear flake prices have fallen by €250/tonne since the beginning of May, clear food-grade pellet prices are down by €200/tonne and coloured flake prices have fallen by €100/tonne.

Demand remains extremely low as a result of competition from the falling cost of virgin PET and competitively-priced imports from the Far East. Furthermore, the soft drinks sector has failed to raise seasonal demand in line with expectations due to the summer weather being less than favourable than usual in Europe.

Material availability is more than sufficient despite recyclers continuing to curb production while imports have added to the growing supply surplus.

R-PET prices are likely to fall further in July due to continuing low demand and competition form the lower cost of virgin material.

Recycled high-density polyethylene (R-HDPE)

R-HDPE prices have fallen in each of the last two months due to weak demand and plentiful supply. R-HDPE blow moulding prices have declined by a total of €80/tonne since the beginning of May while injection moulding grade prices fell by €40/tonne over the same period.

Demand remains extremely low and recyclers have responded by curbing output even more to avoid a further build-up of stocks.

In July, R-HDPE prices are expected to fall again as the start of the holiday season puts additional downward pressure on demand.

Recycled low-density polyethylene (R-LDPE)

R-LDPE prices continued on a downward trend during May and June. R-LDPE natural film prices have fallen by €60/tonne over the last two months, with translucent film prices down by €80/tonne and black extrusion pellet prices down €10/tonne.

R-LDPE film prices were adversely impacted by ongoing weak demand and continued replacement by lower cost, off-spec virgin material from post-industrial sources. Recyclers are increasing production curbs to avoid build-up of excess stock levels, yet availability of base material and recyclate still exceeds demand.

Recycled polypropylene (R-PP)

R-PP prices have fallen in each of the last two months because of low demand, high stocks at recyclers, competition from

the lower cost of off-spec virgin material and lower base material costs. R-PP homopolymer prices have fallen by €100/tonne since the beginning of May while R-PP copolymer prices are down by €90/tonne over the same period. Some recyclers even granted triple-digit price concessions to clear stocks.

In July, R-PP prices are set to soften even further as the start of the holiday season exerts additional downward pressure on demand.

sustainableplastics