Recycled engineering polymer market demands and action plans

Iranpolymer/Baspar the waste and the end-use markets for recyclate. With an evaluation of the evolving legislative environment, it allows for visibility on the current and future status of the market.

The regulatory landscape for plastics recycling is a critical driving force to incentivise the development of sustainability and recycling initiatives in Europe. The main focus is currently on single-use and commodity plastics, with ambitious targets set. However, to achieve the EU’s aim to become net-zero by 2050, aspirations will soon need to reach beyond this to more challenging plastic applications.

Already the Circular Economy Action plan has proposed mandatory requirements for recycled content and waste reduction measures in three product areas of packaging, construction materials and vehicles. In July 2023 , the EU Commission proposed updates to the End-of-Life Vehicle (ELV)

Directive that focus on key elements to improve design, collection, recycling and reporting. Included in this is a target that recycled plastics account for at least 25% of plastics in new vehicles, of which 25% is from recycled ELVs. It is expected that this target cannot be met without the utilisation of recycled engineering polymers, along with significant investment in technologies to make the waste available from end-of-life vehicles.

Based on the current protocol and guidelines for EU construction and demolition waste as well as further data collection initiatives, it can also be assumed that collection, sorting and mandatory recycled content requirements will be introduced for building and construction materials in Europe in the future. The Waste Electrical and Electronic Equipment (WEEE) Directive is also currently being evaluated to assess if it is fit for purpose, can be simplified or if a full review is needed, with a report due in March 2024.

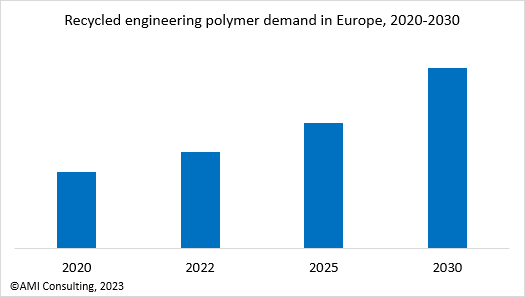

Increasing demand for engineering polymer recyclate presents a multitude of opportunities for innovation, growth and investments in an area with lower volumes, but higher value products. It is predicted that capacity will need to increase by 344kT before 2030 to keep up with demand in Europe.

These polymers are used in diverse and small-scale applications, with only limited volumes available on the market, creating barriers to accessing post-consumer recycling streams. In addition, the quantity and quality of recyclate from key applications must be improved for further utilisation with high specification requirements. Chemical recycling projects for engineering polymers are developing globally, with different levels of commercial availability, where different advanced recycling technologies are suited to processing the different polymers. While pyrolysis technologies do not present the best solution for engineering thermoplastics, several companies have shown that the hydrocarbon output is a possible source for new engineering polymer production. The report analyses the challenges that arise for both the mechanical and chemical recycling of engineering polymers that the industry will need to collaborate on to overcome.

In preparing the report, AMI’s detailed in-house data on virgin polymer demand, polymer end-use applications, and recycling capacities was combined with an extensive research programme including conversations with a wide range of industry participants.

“An Introduction to the Recycling of Engineering Polymers” is a comprehensive report written by Senior Research Analyst, Olivia Poole. This report offers valuable insights into the mechanical recycling capacity of engineering polymers in Europe, while also highlighting global chemical recycling activities. Additionally, it provides a quantitative analysis of the demand for individual engineering polymer recyclates.

industrysourcing