Defossilising the chemical industry: Role of chemical recycling

Iranpolymer/Baspar At the Renewable Materials Conference 2024 organised by nova-institute, the overarching theme this year was the defossilisation of the chemicals and materials industry. The industry is one that is heavily dependent on fossil fuels, with currently 88% of the carbon being sourced from fossil resources – in other words, defossilisation has the potential to make real impact.

Getting there, however, is easier said than done. Sreepna Das provided reporting from the conference.

Finding alternative carbon sources

Dimitri Daniels, VP of Chemical Recycling & Upgrading at GreenDot and a speaker at the conference, got it exactly right when he concluded his presentation with the message that “It is not mechanical versus chemical recycling… instead… it is recycled versus fossil!”

He also shared his company’s plans for leveraging both mechanical as well as advanced recycling to ensure that recycled content will be available in time for the plastic packaging market in Europe. Among others, he noted that Green Dot’s growing assets base currently spans five sorting and recycling sites across Europe, including a 90 kt input capacity plant, currently under construction in Austria as well as a

33 kt input capacity chemical recycling plant in France, which is currently under construction.

Chemical recycling

A dedicated session on ‘Mechanical, Physical, and Chemical Recycling’ was held on the second day of the conference featuring presentations from technology providers within the advanced recycling space: Aduro Clean Technologies, BioBTX, BlueAlp,and matterr RITEC.

Aduro Clean Technologies, one of the nominees for the Innovation Award this year, differs from the usual pyrolysis process – which was the reason this technology was named a finalist, becoming the sole advanced recycling technology to make the shortlist.

In his presentation, Eric Appelman, Chief Revenue Officer at Aduro Clean Technologies introduced Aduro’s innovative technology to the audience. Among the benefits he discussed was the fact that Aduro uses a low-cost catalyst to break down polyolefins at a much lower temperature than in pyrolysis. “This lower temperature makes it possible to achieve two other important reactions: first, the in-situ conversion of the hydrocarbon fragments to make alkanes rather than olefins, which must be hydrogenated afterward. And second, the hydrolysis of PET and nylon, enabling elegant removal of their oxygen and nitrogen heteroatoms, which would require pre-sorting and post-processing otherwise,” he said.

He also emphasised the technology’s potential to enhance the financial viability of advanced recycling, due to the strong reduction in the formation of char and fuel gas. “As a consequence, feedstock specifications can be more forgiving and the need for post-treatment is much less,” he explained.

Strong growth projected

Chemical recycling, although still a nascent technology, is expected to rapidly gain momentum in the next 5 years. With the construction of various projects in progress and plans for others announced the technology is gearing up for the future. A report published earlier this year by nova-Institute under the title Mapping of advanced plastic waste recycling technologies and their global capacities’ covered over 340 installed and plants already in operation, including such details as the product yields potential and capacities of each.

According to this report, global capacity globally is expected to double and in Europe, it is likely to quadruple by 2027. Technology-wise, pyrolysis is expected to show the strongest growth followed by solvolysis.

However, living in a VUCA – volatile, uncertain, complex, and ambiguous- world means that uncertainty rules. Cases where plans of establishing commercial-scale advanced recycling plants have gotten delayed. The ambiguity regarding the policy framework has been another barrier, impeding investments and suppressing growth.

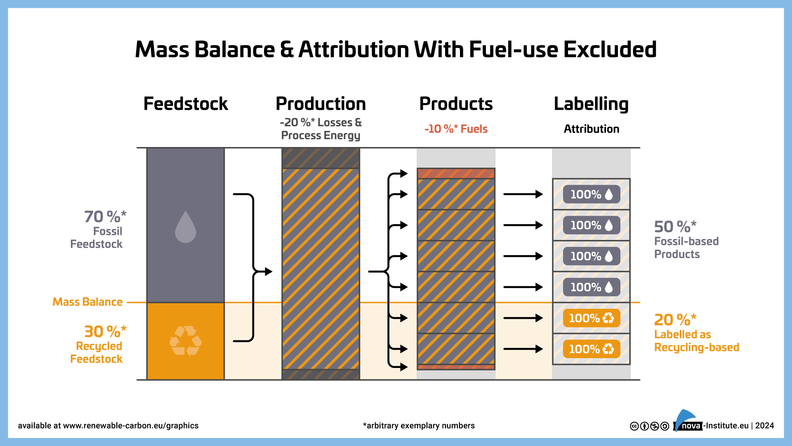

The policy situation, in particular regarding the view taken by the EU on mass balance, however, appears to be poised for change. Mass balance is being intensively discussed within the scope of the Single-use Plastics Directive (SUPD).

The mass balance approach allows credits to be transferred from outputs of the categories ‘plastics’ and ‘other materials’ to high-value polymer output, but not from ‘fuel output’. With the acceptance of this model, chemical recycling could contribute to the recycled content quotas set by the Packaging and Packaging Waste Regulation.

Although a universal and standardised mass balance approach does not yet exist, ISO is currently developing a new mass-balance standard – ISO/CD 13662, which will put in place requirements and guidelines for its use, including rules on attribution limits, transparency and communication. Its acceptance and its impact on the recycled content targets set out by the Packaging and Packaging Waste Regulation (PPWR) by the EU was a topic of much discussion amongst the participants at the conference.

Textile-to-textile recycling is the way forward

Not just packaging, similar recycled content targets are expected in other sectors such as textiles, automotive, building and construction, and e-waste. Chemical recycling can support the circularity of such complex waste streams. At the conference, there were some interesting presentations from UPM and VAUDE on the current and future status of textile recycling.

Much like the packaging waste problem, managing textile waste is a global problem. Less than 1% of all textiles worldwide are recycled into new products. In the EU alone, 12.6 million tons of textile waste is generated annually!

While there have been advances in incorporating recycled content in synthetic fibres, it still is in the early stages and the majority comes via the bottle-to-textile route – mainly PET bottles. With the -packaging industry strongly focused on closed-loop solutions and the circular use of bottles; the pressure is on the textile industry to focus on textile-to-textile recycling. This is supported by the EU strategy for sustainable and circular textiles as well, which is asking the industry to prioritise fibre-to-fibre recycling.

MEPs in the Environment Committee recently adopted new rules that would set up extended producer responsibility (EPR) schemes for textiles, clothing and footwear. This will help cover the costs for their separate collection, sorting, reuse, and recycling in the EU. New regulations around recycled content targets are also expected.

Takeaways

Chemical or advanced recycling will play a key role in the transition of the chemical industry toward a defossilised and circular future.

sustainableplastics